SECURE 2.0 passed in December 2022, but its provisions have been rolling out in waves ever since. Most of the attention has focused on the legislative changes themselves. Far less attention has gone to a downstream problem that falls squarely on TPAs and payroll providers: the data.

Three SECURE 2.0 provisions now in effect directly change how contribution data must flow from payroll systems to recordkeepers. If your payroll integration was not updated to handle them, contributions are routing incorrectly, compliance exposure is building, and in most cases no one is flagging it.

We explain the three changes, what each one requires at the payroll data level, and what breaks when the integration is not built to handle them.

A Quick SECURE 2.0 Recap

The SECURE 2.0 Act of 2022 expanded on the original SECURE Act of 2019, with over 90 provisions affecting retirement plan administration. While many changes involved plan design, eligibility rules, and Required Minimum Distributions, three provisions have direct implications for how payroll data is classified, routed, and delivered to recordkeepers:

• Super catch-up contributions for participants aged 60 to 63

• Mandatory Roth treatment for catch-up contributions made by high earners

• Expanded automatic enrollment requirements for new plans

Each of these creates a specific technical requirement at the payroll integration layer. Here is what that looks like in practice.

Super Catch-Up Contributions (Ages 60 to 63)

What Changed

Section 109 of SECURE 2.0 created a new "super catch-up" contribution limit for participants aged 60 through 63. For plan years beginning after December 31, 2024, these participants can contribute the greater of $10,000 or 150 percent of the standard catch-up limit, indexed annually for inflation.

For 2025 and 2026, the standard catch-up limit is $7,500. One hundred fifty percent of that is $11,250, which exceeds $10,000, so the super catch-up limit is $11,250. This is a meaningful increase above what participants aged 64 and older or under 50 can contribute.

Key distinction: the super catch-up applies only to participants who are age 60, 61, 62, or 63 during the calendar year. Participants who turn 64 revert to the standard catch-up limit.

What It Requires From Payroll

To administer the super catch-up correctly, payroll systems and their integrations must:

• Track each participant's age in the current plan year

• Apply the correct catch-up limit based on whether the participant falls in the 60 to 63 age window

• Map contributions to the correct money type or contribution code at the recordkeeper, which may differ from the standard catch-up code

The age tracking piece is where most problems begin. Payroll systems that relied on a single catch-up contribution code and a flat IRS limit now need to differentiate between participants based on age, and route contributions accordingly.

What Breaks Without the Right Integration

If the integration does not account for the super catch-up, contributions from 60 to 63-year-old participants may be capped at the standard $7,500 limit, meaning participants miss out on up to $3,750 in additional contributions they are legally entitled to make. Alternatively, contributions may route to the wrong money type at the recordkeeper, creating reconciliation problems and potential compliance exposure.

Guidance: IRS Notice 2024-2 provides detailed guidance on super catch-up contributions under SECURE 2.0.

The Roth Catch-Up Requirement: A Payroll Data Classification Problem

What Changed

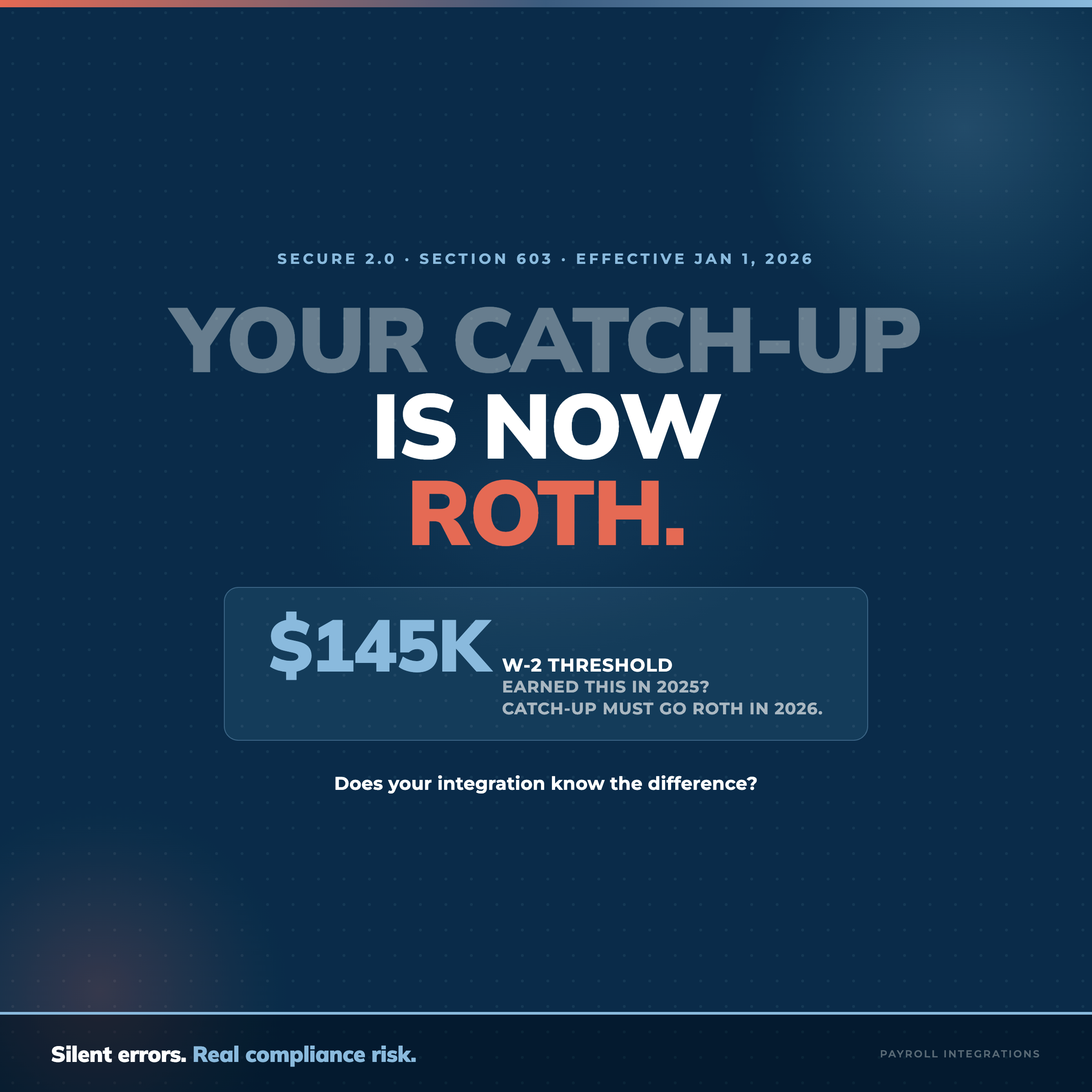

Section 603 of SECURE 2.0 requires that catch-up contributions made by participants who earned $145,000 or more (indexed for inflation) in prior-year W-2 wages from the same employer must be designated as Roth contributions. Pre-tax catch-up contributions are no longer permitted for this group.

After a two-year administrative transition period established by IRS Notice 2023-62, this requirement became effective January 1, 2026. Plans that are not in compliance are at risk of disqualification.

Who Is Affected

The $145,000 threshold applies to W-2 wages earned in the prior calendar year from the same employer that sponsors the plan. This means:

• A participant who earned $145,000 or more in 2025 must make all catch-up contributions as Roth in 2026

• A participant who earned less than $145,000 in 2025 may continue making pre-tax catch-up contributions in 2026

• The threshold is re-evaluated each year based on prior-year W-2 wages

This is not a one-time setup. The Roth catch-up determination must be made each plan year, for each participant, based on updated prior-year compensation data.

What Payroll Systems Need to Track

To comply, payroll systems and their integrations must:

• Have access to prior-year W-2 compensation data for each participant

• Flag participants at or above the $145,000 threshold

• Automatically route their catch-up contributions to a Roth catch-up contribution code rather than a pre-tax catch-up code

• Map those codes correctly to the corresponding money types at the recordkeeper

What Breaks Without the Right Integration

This is one of the highest-risk SECURE 2.0 provisions from a payroll data perspective because the failure mode is silent. If catch-up contributions for a high earner continue to route as pre-tax, the contribution lands in the wrong bucket at the recordkeeper with no automatic alert. The plan is technically out of compliance, the participant's tax treatment is incorrect, and neither party may know until an audit or year-end reconciliation surfaces the discrepancy.

The critical factor: different payroll systems use different contribution codes for Roth catch-up. ADP's Roth catch-up code is not the same as Paylocity's, which is not the same as Paychex's. Without an integration that was built with the right code mapping for each payroll system, contributions will route incorrectly regardless of how well the plan document is written.

Guidance: IRS Notice 2023-62 and IRS Notice 2024-2 provide the administrative framework for the Roth catch-up requirement.

Expanded Automatic Enrollment: A Deferral Setup Problem

What Changed

Section 101 of SECURE 2.0 requires that most new 401(k) and 403(b) plans established after December 29, 2022 include automatic enrollment. The requirement became effective for plan years beginning after December 31, 2024.

Under the mandate, plans must automatically enroll eligible participants at a deferral rate between 3 and 10 percent, and automatically escalate contributions by 1 percent per year until the rate reaches at least 10 percent, but no more than 15 percent. Participants may opt out or change their rate at any time.

Why It Creates a Payroll Data Challenge

Automatic enrollment shifts the default from "do nothing" to "act unless you opt out." That change sounds simple at the plan design level. At the payroll integration level, it creates a deferral setup problem.

When a new employee becomes eligible under an auto-enrollment plan, the recordkeeper needs to communicate the enrollment and initial deferral rate back to the payroll system so the correct deduction is set up before the first eligible pay cycle. If that communication does not happen automatically, the deferral either does not start on time or has to be set up manually, which scales poorly in a plan with dozens of employers and hundreds of new hires per year.

For MEP and PEP sponsors, the auto-enrollment problem is compounded across every participating employer. A plan with 40 employers onboarding new employees on different cycles creates 40 separate data flow requirements, each of which needs to work correctly every pay period.

For a deeper look at how multi-employer plan structures create payroll data challenges beyond auto-enrollment, see our full guide to MEP and PEP payroll data.

What Breaks Without the Right Integration

If the payroll integration does not support the bidirectional data flow required for auto-enrollment, common failure modes include:

• Deferral deductions not starting until a manual intervention is made, leaving participants without contributions for one or more pay cycles

• Auto-escalation percentages not updating in the payroll system when the recordkeeper triggers the annual increase

• Opt-out elections at the recordkeeper not routing back to payroll, resulting in continued deductions for participants who elected to opt out

Each of these failures creates a compliance issue and erodes participant trust.

What TPAs Should Ask Their Payroll Integration Vendor

If you work with payroll providers and want to confirm that their integrations are handling these SECURE 2.0 changes correctly, here are the questions to ask:

• Has your integration been updated to support super catch-up contributions for participants aged 60 to 63? Which payroll systems and recordkeepers is this live for today?

• How does your integration handle the Roth catch-up requirement? Does it access prior-year W-2 compensation data, and how is the $145,000 threshold applied per participant?

• What happens when a catch-up contribution routes to the wrong bucket? Is there an automated alert, or does someone have to find it?

• Does your integration support bidirectional data flow for auto-enrollment? Specifically, can deferral setup and escalation changes route from the recordkeeper back to the payroll system automatically?

• How are SECURE 2.0 contribution code mappings maintained across different payroll systems? Is this done manually or is it part of the integration infrastructure?

How Payroll Integrations Supports SECURE 2.0 Compliance

Payroll Integrations builds and maintains direct API connections between payroll systems and recordkeepers. Our integrations are purpose-built for retirement plan compliance, which means SECURE 2.0 changes are addressed at the integration infrastructure level, not as one-off customizations for each plan.

Across our network of 75+ payroll systems and 75+ recordkeepers, we have updated contribution code mappings to support super catch-up and Roth catch-up classification, and our bidirectional data flow architecture supports the auto-enrollment deferral setup loop required by Section 101.

If you work with a payroll provider that is not yet on our network, or if you are evaluating integration vendors for a new plan, see our full list of payroll partners or reach out to our team directly.

The Bottom Line

SECURE 2.0 is not just a plan design update. It is a payroll data infrastructure challenge. Super catch-up contributions require age-based classification. The Roth catch-up mandate requires prior-year compensation tracking and correct code mapping. Expanded auto-enrollment requires bidirectional data flow between the recordkeeper and the payroll system.

Each of these requirements depends on the integration layer working correctly. And in most cases, a failure at that layer is silent — no alert fires, no one calls, and contributions continue routing to the wrong place until someone looks.

TPAs who understand this have a significant advantage when advising plan sponsors and evaluating their technology stack.

Want to see how Payroll Integrations handles SECURE 2.0 compliance across your plan's payroll systems? Schedule a demo and we will walk through your specific setup.