The pitch for pooled employer plans is compelling. A Pooled Employer Plan (PEP) or Multiple Employer Plan (MEP) lets small and mid-sized businesses access institutional-quality 401(k) benefits without the administrative burden of running their own plan. One fiduciary. One recordkeeper. Shared costs. Streamlined compliance.

What the pitch leaves out is what happens on the payroll side.

Every employer in a MEP or PEP runs payroll differently. Different providers. Different schedules. Different deduction codes. Different file formats. And every single one of them has to feed clean, consistent data to the same recordkeeper, on time, every pay period.

This is the operational challenge that defines whether a MEP or PEP actually delivers on its promise, and it is the one that almost nobody talks about until something goes wrong.

The Growth of Pooled Employer Plans

The SECURE Act of 2019 and SECURE 2.0 of 2022 opened the door for PEPs by eliminating the "nexus" requirement that once forced MEP employers to share a common bond. Any unrelated business can now join a pooled plan administered by a licensed Pooled Plan Provider (PPP).

PEP assets are growing rapidly. What started as a niche product for large associations is now attracting serious interest from TPAs, broker-dealers, and financial institutions looking to serve the small-to-mid market at scale.

The operational infrastructure required to support that growth, however, has not kept pace with the enthusiasm.

Managing Multiple Payroll Systems in a Pooled Employer Plan

In a traditional single-employer 401(k) plan, the data flow is relatively straightforward: one payroll system sends data to one recordkeeper. When something breaks, there is one integration to diagnose.

In a MEP or PEP with 40 participating employers, you have 40 payroll systems feeding data into a single recordkeeper. Each employer uses whatever payroll provider they already have: ADP, Paychex, iSolved, Paylocity, QuickBooks Payroll, and dozens of others. Each system formats data differently. Each has its own API behavior, its own deduction code structure, its own timing.

The Pooled Plan Provider or TPA is responsible for making sure all of it arrives correctly at the recordkeeper, on time, for every pay cycle, for every employer in the plan.

That is not a simple coordination problem. It is a continuous data infrastructure challenge.

Four Payroll Data Problems That MEPs and PEPs Cannot Afford to Ignore

1. Inconsistent Payroll Schedules and Timing

Employers in a pooled plan do not all run payroll on the same schedule. Some pay weekly. Some biweekly. Some semi-monthly. A few may run off-cycle payrolls for bonuses or corrections.

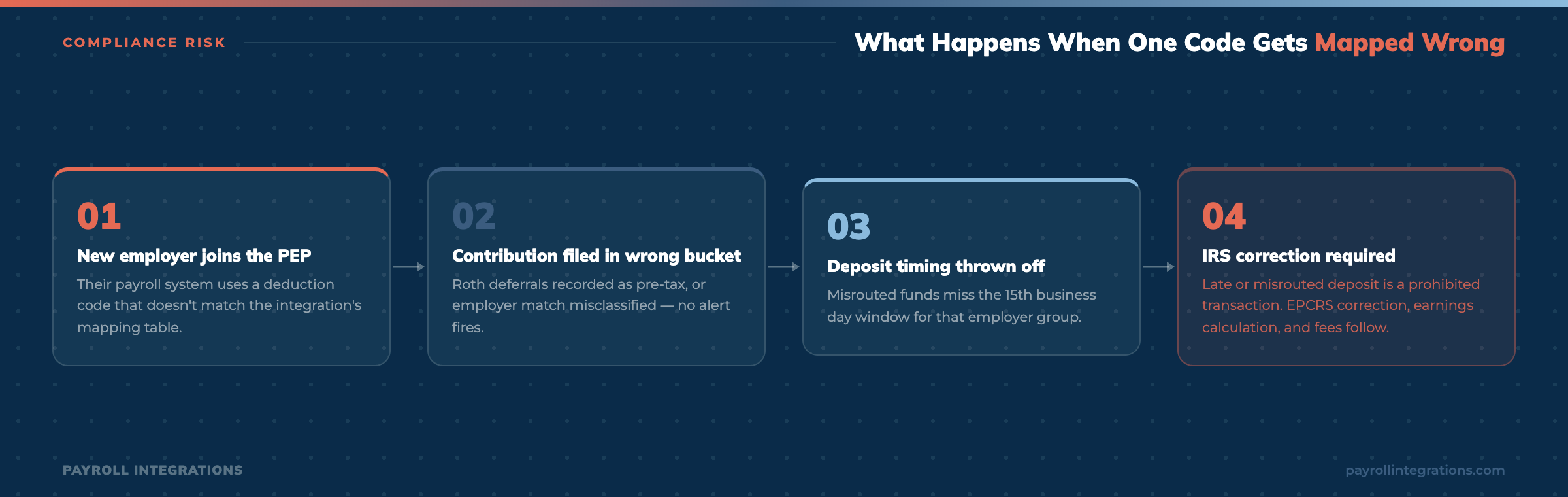

The 15th business day rule for deferral deposits applies to each employer individually, not to the plan as a whole. That means the PPP or TPA must track deposit timing across every employer's payroll calendar, not just the plan's. Late deposits from any one employer create an IRS prohibited transaction that applies to that employer, regardless of how cleanly the rest of the plan runs.

2. Contribution Code Mapping Across Every Payroll System

Each payroll system uses its own codes to identify contribution types: pre-tax deferrals, Roth deferrals, employer match, safe harbor contributions, loan repayments. There is no universal standard.

A code that means "Roth 401k" in ADP may have a completely different label in Paychex or iSolved. When a new employer joins a pooled plan, their existing payroll codes need to be mapped to the recordkeeper's expected money types before the first payroll runs. If that mapping is wrong or incomplete, contributions land in the wrong bucket, or do not land at all.

SECURE 2.0 added complexity here. The super catch-up contribution for employees aged 60 to 63, and the mandatory Roth treatment of catch-up contributions for high earners, require payroll systems to support new deduction codes. In a pooled plan, every participating employer's payroll provider needs to handle these correctly, and the PPP needs visibility into whether they do.

3. Employee Census Fragmentation

A recordkeeper managing a PEP needs accurate, current census data for every participant across every employer. That means name, address, date of birth, date of hire, employment status, compensation, and hours. In a single-employer plan, that data comes from one source. In a pooled plan with 40 employers, it comes from 40 separate payroll systems, each maintaining its own records in its own format.

When an employee gets married and changes their name, or terminates and is rehired, or moves to a different division, that update needs to make it from the employer's payroll system to the recordkeeper. In a pooled plan, the opportunity for that data to fall through the cracks is multiplied by every employer in the plan.

Missing or stale census data causes enrollment delays, incorrect vesting calculations, and compliance issues at year-end.

4. Deferral Rate Changes That Do Not Make It Back to Payroll

This one runs in the opposite direction, and it is the challenge most often overlooked.

When a participant logs into the recordkeeper's portal and changes their deferral rate, that change needs to flow back to their employer's payroll system before the next pay cycle. In a single-employer plan, that is one integration to manage. In a MEP or PEP, every deferral change for every participant needs to route back to the correct employer's payroll provider

If that return path does not exist, the participant's paycheck is unchanged. The recordkeeper shows one rate; payroll shows another. Neither system flags the discrepancy. The participant notices months later, if at all.

This Is a Compliance Problem, Not Just an IT Problem for MEPs and PEPs

The payroll data challenges inside a MEP or PEP are not abstract technical issues. They have direct compliance implications.

Late deferral deposits trigger prohibited transaction rules. Contribution miscoding creates that require correction under IRS Employee Plans Compliance Resolution System (EPCRS) programs. Missing census data affects eligibility and vesting determinations. Deferral changes that do not reach payroll mean participants are not getting what they elected.

A Pooled Plan Provider carries fiduciary responsibility for plan administration. When payroll data breaks down, the consequences land on the PPP, not just the employer whose system caused the problem. The quality of the payroll data infrastructure is, in effect, a fiduciary risk management decision.

MEP and PEP growth is being driven by the promise of operational simplicity. The PPPs and TPAs that will win long-term are the ones who solve the payroll data problem before it becomes a liability.

What Purpose-Built Infrastructure Looks Like for MEPs and PEPs

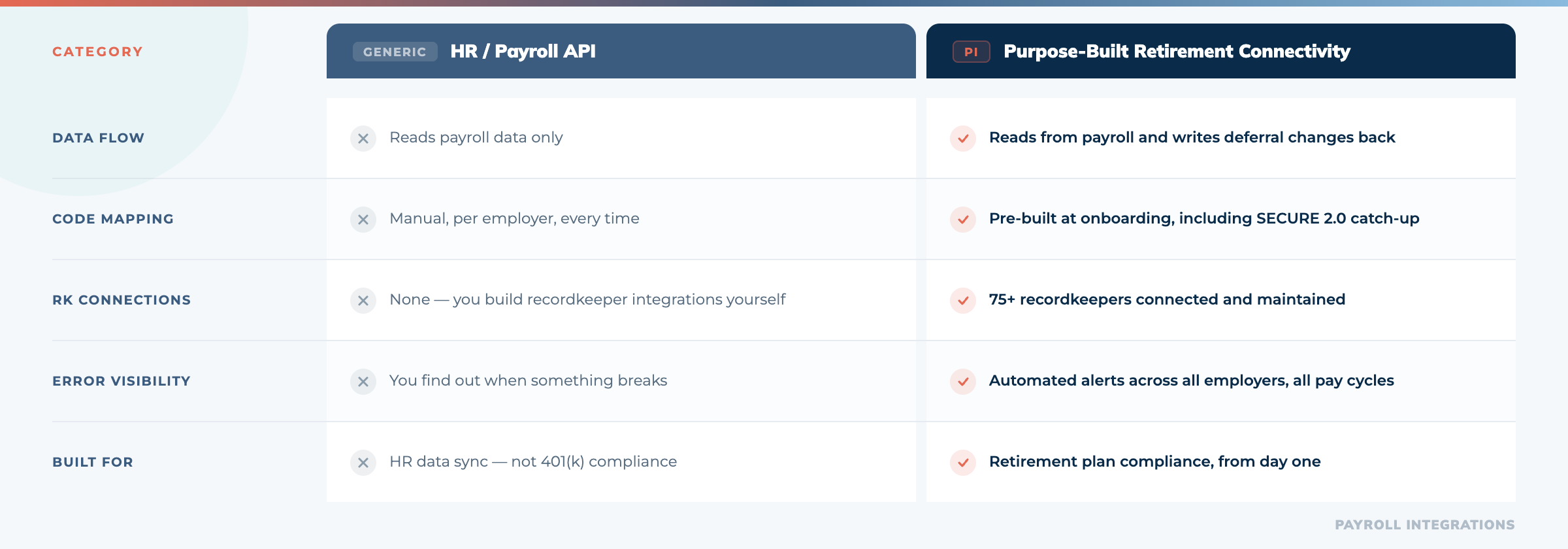

Solving the payroll data challenge in a MEP or PEP requires more than a generic API connection to payroll systems. It requires:

- Bidirectional sync: data flowing from each employer's payroll to the recordkeeper, and deferral changes flowing back from the recordkeeper to each employer's payroll.

- Pre-built recordkeeper connections: not just the ability to connect to any API, but established, tested relationships with the recordkeepers that actually serve MEP and PEP plans.

- Contribution code mapping expertise: the ability to map each employer's deduction codes to the recordkeeper's money types correctly at onboarding, and to update those mappings as payroll systems change or SECURE 2.0 requirements add new contribution types.

- Census data normalization: the ability to pull employee data from any payroll system and deliver it to the recordkeeper in the expected format, consistently.

- Operational visibility: the PPP or TPA needs to see when a file failed, when a mapping is missing, when a deferral change did not complete, without having to log into 40 different systems to find out.

A unified API platform that reads employment data from payroll systems is a different product than a purpose-built 401(k) payroll connectivity solution. The former is designed for developers building HR software. The latter is designed for the compliance-sensitive, recordkeeper-specific reality of retirement plan administration. Pooled plans need the latter.

The Question to Ask Your Integration Vendor

When evaluating payroll integration infrastructure for a MEP or PEP, one question cuts through most of the noise:

"When a participant changes their deferral rate at the recordkeeper, how does that change get back to their employer's payroll system, and how do you know it worked?"

A vendor with generic API connectivity will struggle to answer that question specifically. The answer requires knowing how each recordkeeper surfaces deferral changes, how each payroll provider accepts them, and what happens when the loop does not close.

That is the operational detail that separates a tool from an infrastructure partner.

The Bottom Line

MEPs and PEPs are the right product for the small and mid-market. They offer real cost advantages and real compliance efficiencies. But the promise of a pooled plan only holds if the payroll data flowing into it is accurate, complete, and timely, from every employer, every pay period.

The Pooled Plan Providers and TPAs building durable businesses in this space are not just choosing a recordkeeper and a fund lineup. They are choosing payroll infrastructure that can scale with the plan, handle every employer's payroll system, and keep data clean as the participant base grows.

That infrastructure choice is worth getting right before the first employer joins.

If your current workflow relies on file exports, manual reconciliation, or periodic syncs, we should talk.

Payroll Integrations connects 200+ payroll providers to 80+ recordkeepers through purpose-built, bidirectional integrations designed for the compliance requirements of 401(k) plans. If you are building or growing a MEP or PEP, we would be glad to walk through how we support pooled plan infrastructure.